University funding is one of those subjects that looks straightforward until you start asking questions, then it quickly becomes a rabbit hole.

University funding is one of those subjects that looks straightforward until you start asking questions, then it quickly becomes a rabbit hole.

Last month, in Education, Money & The Long View of Time, we explored university fees and questions beyond the financial ones – revolving around not only how to pay for education, but what it means for:

- The desire to give opportunities to the next generation without creating dependency

- The fear of making a choice that could limit your own future security

- Fairness between children

In this article, we dive more into the detail – setting out the practical mechanics of student loans and looking at scenarios to show options over time.

Not all student loans are equal

The thing with student loans is that not all loans are equal. UK student loans operate across five distinct repayment plans, each determined by when and where a borrower studied (not where they live or work now).

- Plan 1 covers those who began undergraduate study in England or Wales before September 2012, or in Scotland and Northern Ireland under older arrangements.

- Plan 2 applies to English and Welsh students who started between 2012 and 2023

- Plan 4 covers Scottish-domiciled borrowers funded through SAAS

- Plan 5 applies to students in England starting from August 2023 onwards, with repayments beginning no earlier than April 2026.

- A postgraduate loan, sometimes incorrectly labelled Plan 3, sits alongside these for master’s and doctoral borrowers.

How the numbers have changed

A student who started in 2011 borrowed a fundamentally different amount from one who started in 2013, and this gap compounds over a repayment period that can stretch across decades.

University tuition fees in England illustrate the point:

- In 2011 tuition fees were £3,290 per year

- By 2013, fees had tripled to £9,000 per year

- Today they rise annually with inflation, reaching £9,790 for 2026/27

Interest rates on loans

It is not just the difference in university tuition fees to consider, but the interest rate charged on the loan that could widen the gap further.

In the UK, each loan plan has its own rules. Some rise each year with the Retail Price Index (RPI), whilst others can increase by RPI +3%.

The critical differences between plans lie in three parameters:

- The income threshold at which repayments begin

- The interest rate applied to the outstanding balance

- The period after which any remaining debt is written off

Current loans are Plan 5, with interest set at RPI only (no extra premium added).

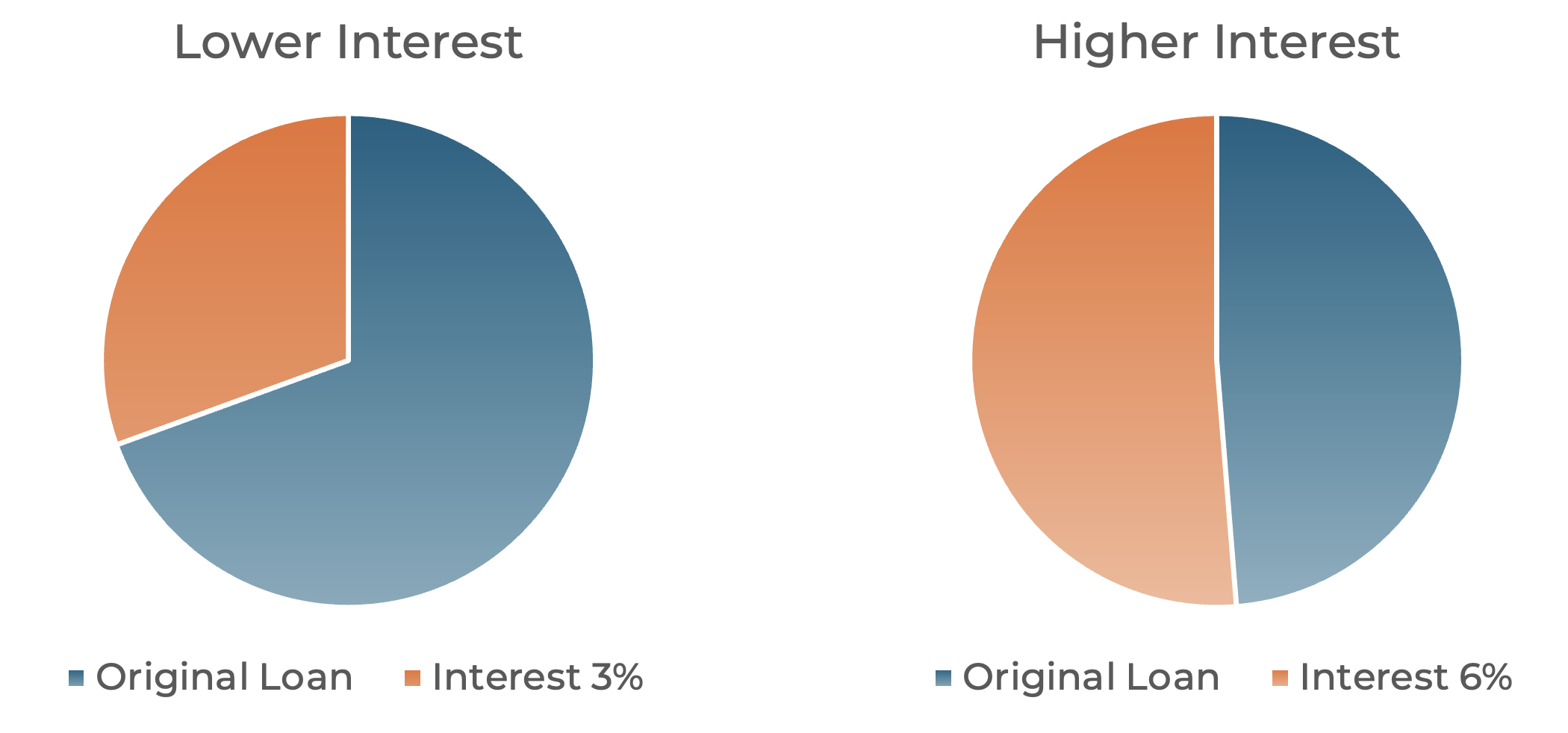

Brought to life: the higher interest rates difference

Emily left university with a £30,000 loan.

After 14 years, the loan with 6% interest rate has grown to be more than the original loan and sharply reflects the compounding effect for loans with higher interest rates applied – a clear example of how higher rates compound over time.

The chart below illustrates how the same £30,000 loan diverges over 15 years when interest is applied at 3% versus 6%.

Repayment periods

Different plan types also have different maximum repayment periods before they are effectively written off – this initially was 25 years in 2011 but has increasedto 40 years now.

This extended repayment period is a trade-off against interest rates reducing to just RPI but sentences graduates to repaying loans for almost the entirety of their working lives.

Repayment amount

Plans 1, 2, 4, and 5 each require repayment of 9% of income (above their respective thresholds), while postgraduate borrowers repay at 6%.

Maintenance Loans

Students have the option to take out loans for maintenance as well as tuition, to pay for accommodation and living costs.

Unlike tuition loans, they are means-tested, and the maximum entitlement can exceed the tuition fee loan in value.

In 2025/26:

- Tuition fees in England will be £9,790

- The maximum maintenance loan is £14,135

- This gives a combined maximum of £23,925 per year of study

Over a standard three-year degree, total borrowing can therefore exceed £70,000 – and that’s before interest starts to accumulate.

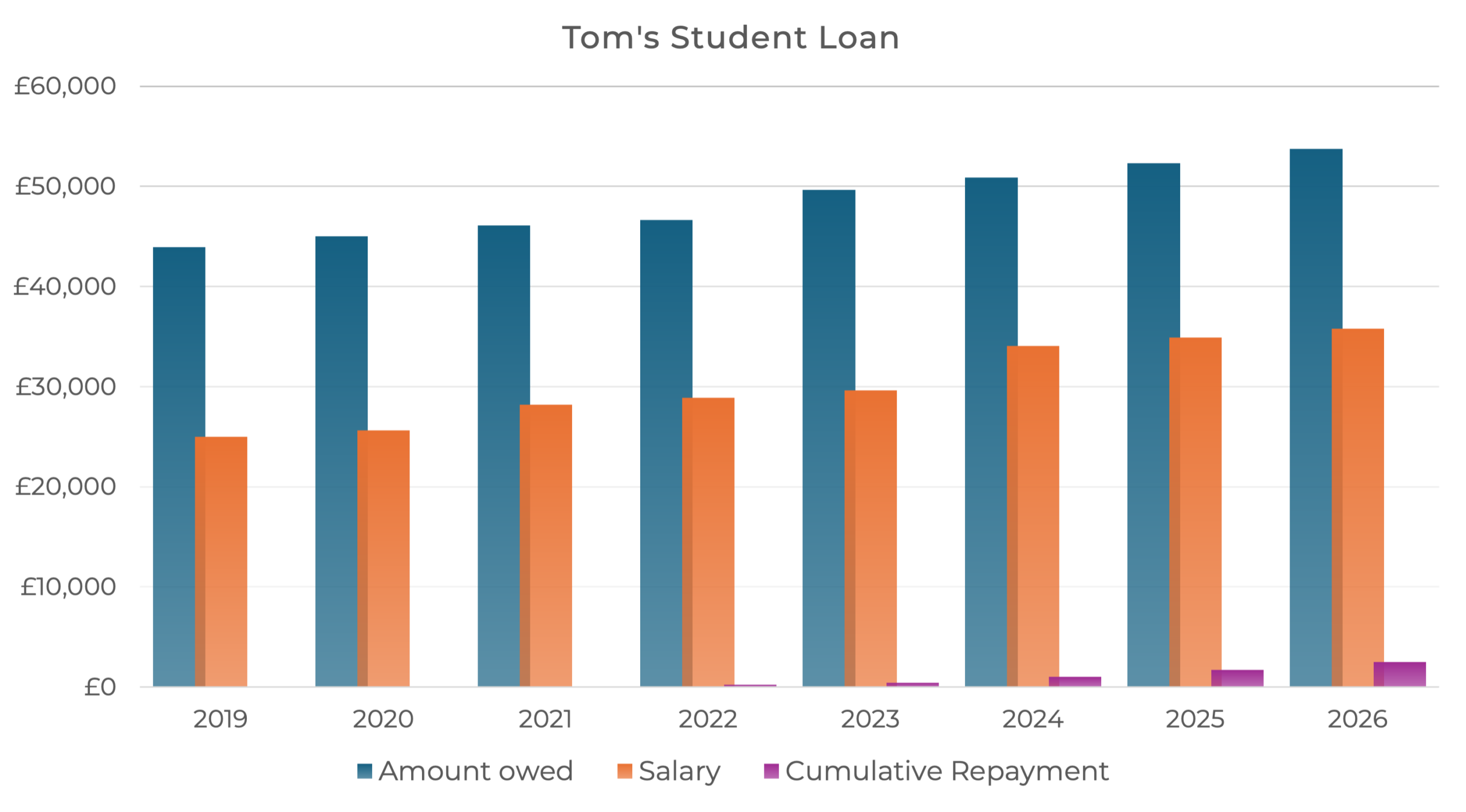

Brought to life – plan 2 loan repayments with average salary

Tom graduated in June 2018, following a three-year degree. He took a Plan 2 loan for fees and a partial maintenance loan, totalling £38,400 over the 3 years.

Tom’s graduate salary is £25,000, in 2019. Over the years his salary increases.

In 2021, Tom earned £28,188, which is above the threshold income of £27,295, set by the government, so he started to repay this loan. The repayment that year was £80.

In 2024 Tom paid £764 towards his loan repayment however, the loan grew by over £2,000 in the same period. As at today, in 2026, he now owes £54,000.

The chart below shows his initial loan at the start as well as what was owed in his final year. The size of the loan continues to rise over time, despite the repayments being made.

The repayments are calculated by taking his income over the threshold and taxing that excess at 9%, much the same way as income tax is deducted from a gross salary.

Graduates getting vocal

It is not surprising to see that graduates are starting to become more vocal about the impact student loans are having on their finances with no visible benefit.

Future governments will need to bear in mind that past graduates laden with additional tax burdens for the remainder of their working life, will have less disposable income – and may start to vote with their feet in the future.

Conclusion

Much like in America, university funding is becoming something that parents will need to think about and plan for. The costs of education have gone from being nominal to now being substantial.

Inevitably, if you are thinking of funding university the following points are worth pondering:

- How do we help the younger generations understand the cost of education and enable them to make rational choices about degree education or alternative options?

- Will gifting money make a material difference to the child or is the gift simply subsidising a possibly poor choice with no economic consequences?

- Are you funding education when perhaps alternative options such as house purchase might provide greater impact.

There are many questions beyond this, such as your retirement plans, what’s affordable for you, children’s career prospects… and many more. All of these we can explore with you, but for a quick catch please see out earlier article, Education, Money & The Long View of Time.

Unique options and choices

As you can see the question around student loans and funding is complex and so requires careful thought and planning.

We are here to support you in these decisions so please reach out to us if you want help with student funding support. For a more detailed summary of the choices you have already made or about to make then we would be delighted to provide more information.

Categories: Financial Planning