We see many families, who, at a certain stage in their lives, begin to look towards the future at what might be left behind for their children, grandchildren and other important people or causes.

However, what you pass on is restricted by rules and thresholds. These haven’t kept pace with the changing landscape or moved with you and your family as your lives evolve.

Let’s look at the impact following the Autumn Statement 2025.

1. Inheritance Tax (IHT) bands are frozen – so the current nil rate band (NRB) remains at £325,000.

£325,000 of an estate is taxed at 0% for each individual. There is an additional relief called the Residents Nil Rate Band (RNRB) which came into effect in 2017 and is capped at £175,000 per person. Eligibility for this is more complex and so there are several “ifs and buts” as to who qualifies. However, if your estate value is greater than £2.35 million, you won’t be able to benefit from this additional allowance.

So why was the budget bad news? The £325,000 and £175,000 have been frozen yet again until 2031, that’s six years from now. Also, the nil rate band had not changed since 2009.

Your estate is likely to grow year on year between 3% and 6% (depending on where it’s invested). So, every year more of your estate is likely to be affected by inheritance tax, simply by default. Not because anything has gone wrong, but because the thresholds have not changed. This gradual paying more tax over time, even if rates don’t change, is referred to as fiscal drag and is in effect a stealth tax.

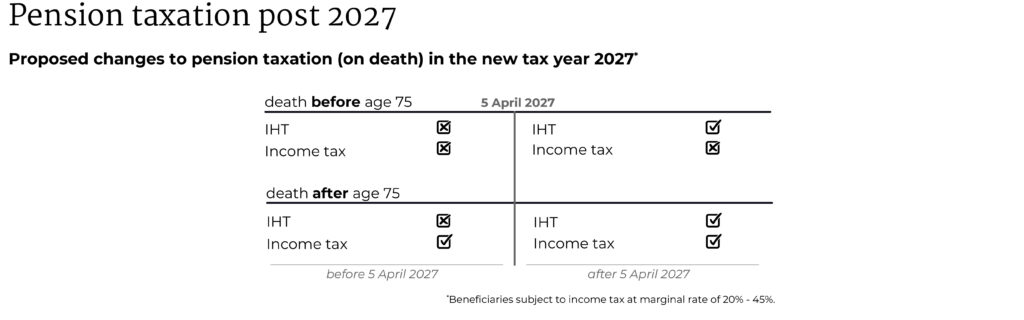

2. From April 2027, unused pensions will form part of your estate – and therefore IHT calculations (This was first raised in the 2024 budget).

For years, pensions have been one of the most effective ways to protect wealth for future generations. But going forwards, inherited pensions, if taken in full, are taxed twice, once by the estate at 40% and a further tax on withdrawal at the beneficiary’s marginal rate of tax.

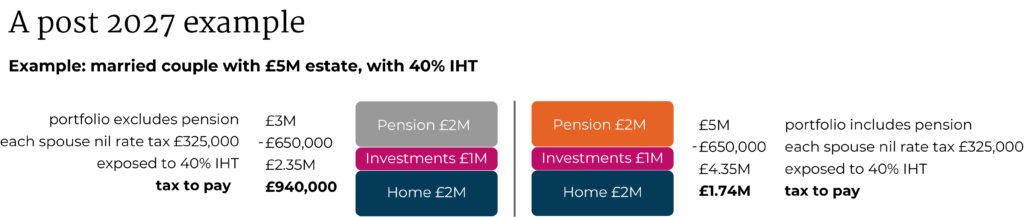

A very simple example here will illustrate that:

Currently, the estate illustrated will have an IHT liability of £940,000. However, this exact same estate, after the changes to the pension regulations in April ‘27, will have an IHT bill of £1.74m. That’s an 85% increase for this particular estate. In addition, beneficiaries will continue to pay income tax at their marginal rate on any withdrawals following the settlement of IHT.

This change doesn’t mean pensions have suddenly become a bad tool, but as legislation changes, our advice to clients will reflect and incorporate these changes.

Mitigating the limitations

The good news is that there are ways in which we can help you mitigate these changes to reduce the effect of fiscal drag:

Gift one nil rate band into trust on first death. That means any growth on that portion between first and second death will not be liable for Inheritance Tax. This gift effectively protects the nil rate band from these frozen thresholds.

A widowed client may have access to the transferable nil rate band from their late spouse, plus a new spouse’s allowance, that makes three nil rate bands that they can make use of. So, to make use of this additional up to £325,000, both partners would need to structure their wills accordingly: either to include an outright gift up to the available nil rate band or via a trust. Using this additional Nil Rate Band available can save an estate up to £130,000 in tax.

Re-consider the order you withdraw from your assets in retirement. It is likely to be better to withdraw from your pension ahead of other assets, such as your ISA or your General Investment Account.

You might be in a position to gift into your children’s or grandchildren’s pensions using the “gifts out of normal expenditure” rule. To qualify for this rule, gifts need to be made regularly from income and not impact your normal standard of living. These particular gifts are immediately exempt from IHT, without waiting for the 7 years, if they meet these three criteria.

There are other practical steps you could take to reduce your liability, which I outline in the video below.

Importantly, families are all unique with their own circumstances. There may be a large family, a single parent family, blended families with children or grandchildren from different partnerships, but they’re all different and they all have different priorities.

At Citywide, our clients genuinely come first. We listen and understand what’s important to your family while navigating known changes, and then design a plan that’s practical and adaptable, so you can plan for your future with as fewer limitations as possible.

![]()

Alison explores these ideas in more detail, in the “Setting your Family Up for the Future” part of our recent webinar, The Budget and Your Life. Click below to watch her 9 minute section.

![]()

by Alison Hutton, Financial Planner

by Alison Hutton, Financial Planner

Categories: Financial Planning, Retirement, Tax